This paper serves as a follow up to our publication,

Taxes Matter: An Introduction to Strategies for Improving After-tax Portfolio Returns, where we explained the sources of taxes (bond income, stock dividends and capital gains) and discussed the three primary techniques for limiting taxes: tax-loss harvesting, gifting highly appreciated stock and the use of municipal bonds. Here, we explore nuances of tax-managed investing as well as more sophisticated techniques, used as appropriate, to maximize after-tax returns.

Tax-Managed Investing: Other Considerations

There are various factors to consider when thinking about client tax exposure:

- Rebalancing. We regularly rebalance portfolios to control risk in portfolios. As stock (higher risk) performance generally outpaces bond (lower risk) performance, rebalancing often entails selling appreciated stock and potentially incurring capital gains and building cash and/or buying bonds. A 2019 study by Vanguard analyzed returns between 1926 and 2018. This study demonstrated a regular process of rebalancing, even with a wide variance in the method of rebalancing, has consistently improved risk- adjusted returns on an after-tax basis.[1] Rebalancing portfolios allows us to remain within a client’s risk objectives. Otherwise, riskier assets would become a larger percentage of a portfolio’s overall asset allocation over time. Realizing capital gains is a necessary evil in the process of risk management.

- Mutual funds versus individual securities. Mutual funds can be an important addition to a client’s portfolio for increasing potential return and/or for managing risk. However, the more a strategy allocates to funds, the more tax control is being ceded to the managers of those mutual funds. Mutual funds typically distribute capital gains/losses and income payments to fund holders at year end. In contrast, holding individual securities provides a valuable tax tool by allowing the investor (as opposed to the fund manager) to determine if and when an unrealized capital gain or loss should be realized. Exchange Traded Funds (ETFs), which may mirror various indices like the S&P 500 or Dow 30, often have lower tax burdens due to lower turnover. However, this is not always the case. An ETF subject to significant redemptions and/or active management (versus passive index replication) may have a significant tax burden comparable to a mutual fund.

- Low-basis stock positions. The difference between the current market price of a security and the cost basis is the gain that will be taxed once the security is sold. While gifting low-basis stock is an ideal strategy, there are times when this is not an option or gifting should be done in conjunction with selling. There are a number of factors to consider before selling or reducing a low-basis stock position.

- What is the overall exposure of a client’s portfolio to the stock? The smaller the position size, the less concern we will have with keeping the portfolio adequately diversified. However, there is also less likelihood of a large unrealized gain. It is the large concentrated positions that typically have the most tax liability associated with them.

- What is the fundamental view of the security? If we have a fundamentally favorable view of a security with a large gain, we would be more inclined to hold some or all of the position and manage around that exposure. However, if we have a fundamentally negative view of a security, a sale or reduction should be considered along with potential tax consequences.

- What is the client’s expected Adjusted Gross Income and gains budget in the tax year? For many of our clients with high tax exposure, we work with their accountants to develop a reasonable gains budget. We review their tax status every year and manage the realization of gains from concentrated positions in the context of the gains budget.

- Managing for step-ups. An important estate planning tool is the step-up provision on a deceased investor’s assets. Upon death, the cost basis of an investor’s taxable portfolio is “stepped up” to the market value, effectively removing the unrealized gain. As clients age and/or their health deteriorates, managing the portfolio for eventual step-up becomes an increasingly important consideration.

- Net Unrealized Appreciation (NUA) of employee stock. We deal with many clients who hold stock of their company within an employer-sponsored retirement plan. The NUA is simply the difference between the cost basis and the current market value (identical to the unrealized capital gain discussed above). The NUA of company stock may be eligible for a more favorable tax treatment if distributed in-kind to a taxable investment account.

- Borrowing against securities. In low interest rate environments, such as the current one, an investment account can sometimes be used as collateral for a loan to fund liquidity needs. The cost of a low interest loan may be preferable to the cost of selling securities with large embedded taxable gains.

- In certain specialized situations, typically involving large concentrated stock positions, stock options may be used to create what is known as a collar. A collar allows ownership of a security to continue (avoiding/deferring taxable gains) while partially mitigating the risk of owning a concentrated position in a single stock.

- Trusts. Trusts can play a critical role in tax management. For estate planning, trusts can offer many advantages including a potential reduction in estate taxes. Trusts can also offer certain tax advantages depending on the state in which they are established. For example, New Hampshire does not impose an income tax on capital gains or dividends and interest earned in an irrevocable trust in which the beneficiaries are non-residents. Speak to a Cambridge Trust representative who can introduce you to our New Hampshire team if you would like to learn more about these trusts.

Location Investing

For our clients who have both taxable and non-taxable or tax-deferred portfolios, there are additional strategies for tax management typically referred to as regime or location strategies. While these strategies are more complex than single account strategies, the rewards can be high. Location strategies consider the tax sensitivity of each security and the tax sensitivity of the security’s investment vehicle. Securities with high tax sensitivity are “located” in tax-deferred investment vehicles and those with low tax sensitivity are “located” in taxable investment vehicles. Client asset allocation is then managed at both the account and the aggregate wealth level.

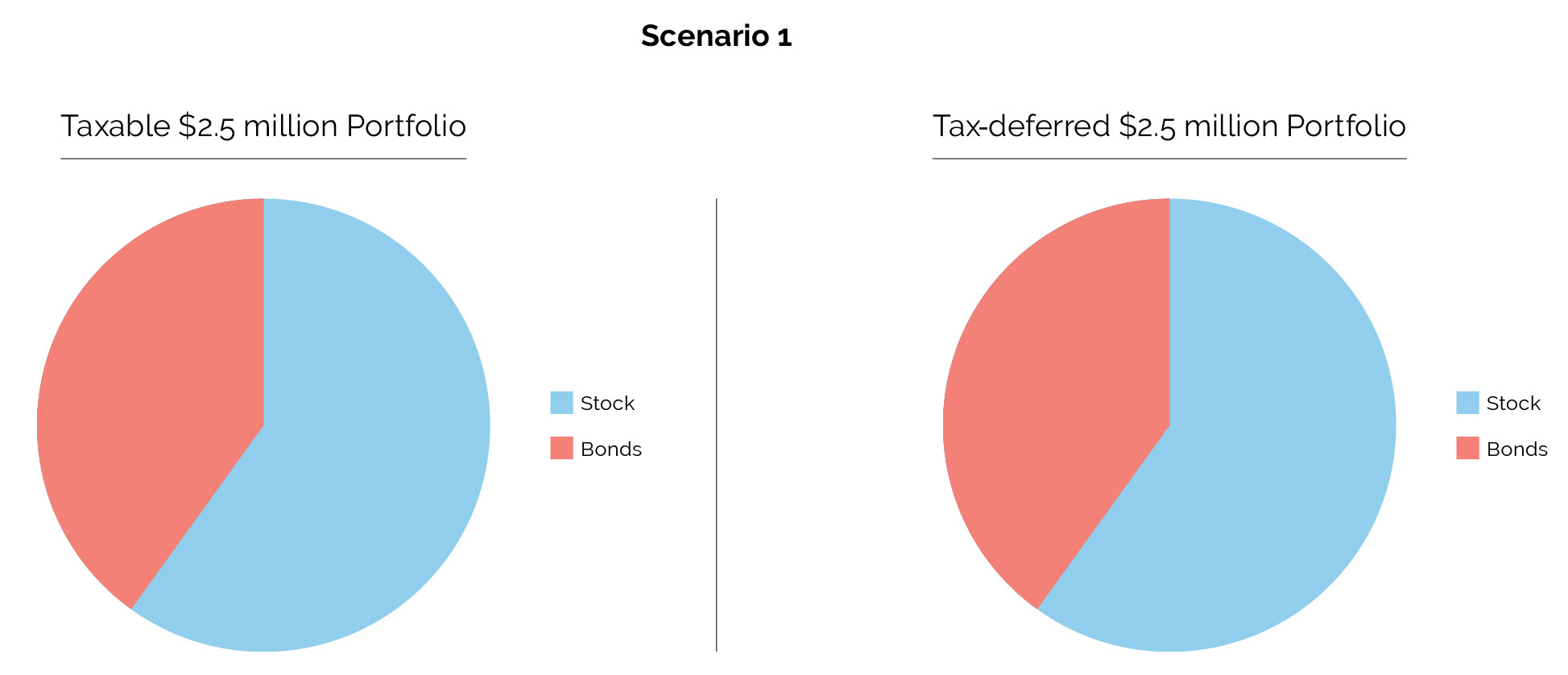

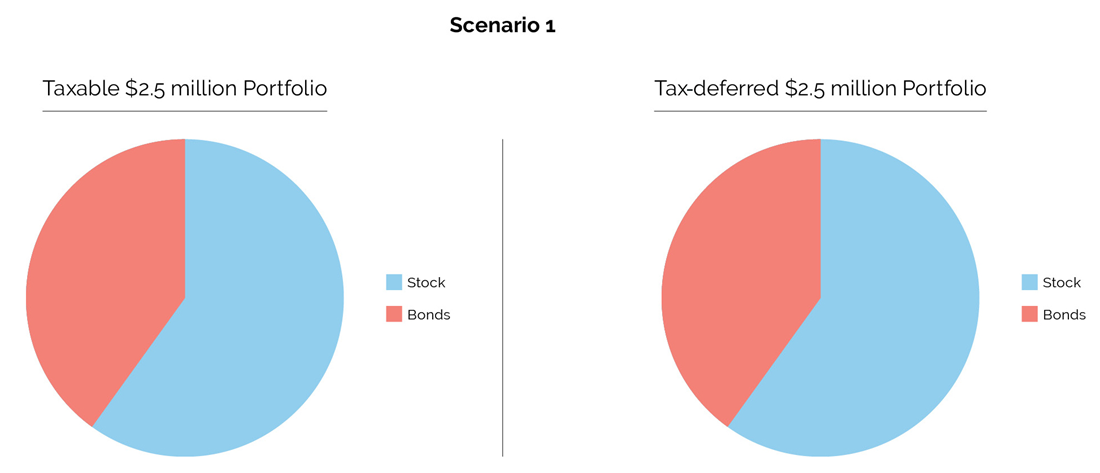

A simple example can demonstrate the power of location investing. A client might have $2.5 million in taxable assets and $2.5 million in retirement (tax-deferred) assets. If the client has a standard 60% stock and 40% bond allocation, the taxable and tax-deferred portfolios might look something like the following portfolios in Scenario 1, with $3 million in stock and $2 million in bonds divided between the two accounts in identical 60% stock/40% bond allocations.

While realized gains would have no tax consequences for stock in the tax-deferred portfolio (assuming no distributions), any gains on the $1.5 million of stock in the taxable portfolio would be subject to capital gains taxation. $75,000 of realized gains

[2] in the taxable portfolio, taxed at 20%, would imply taxes of $15,000

[3]. If the $1 million in bonds in the taxable portfolio are taxable bonds (i.e. not municipals) with a 2% interest rate, they would generate $20,000 in income and be taxed at 42.1%

[4], which would imply taxes of $8,420. In summary, total taxes on realized gains and income would be $23,420.

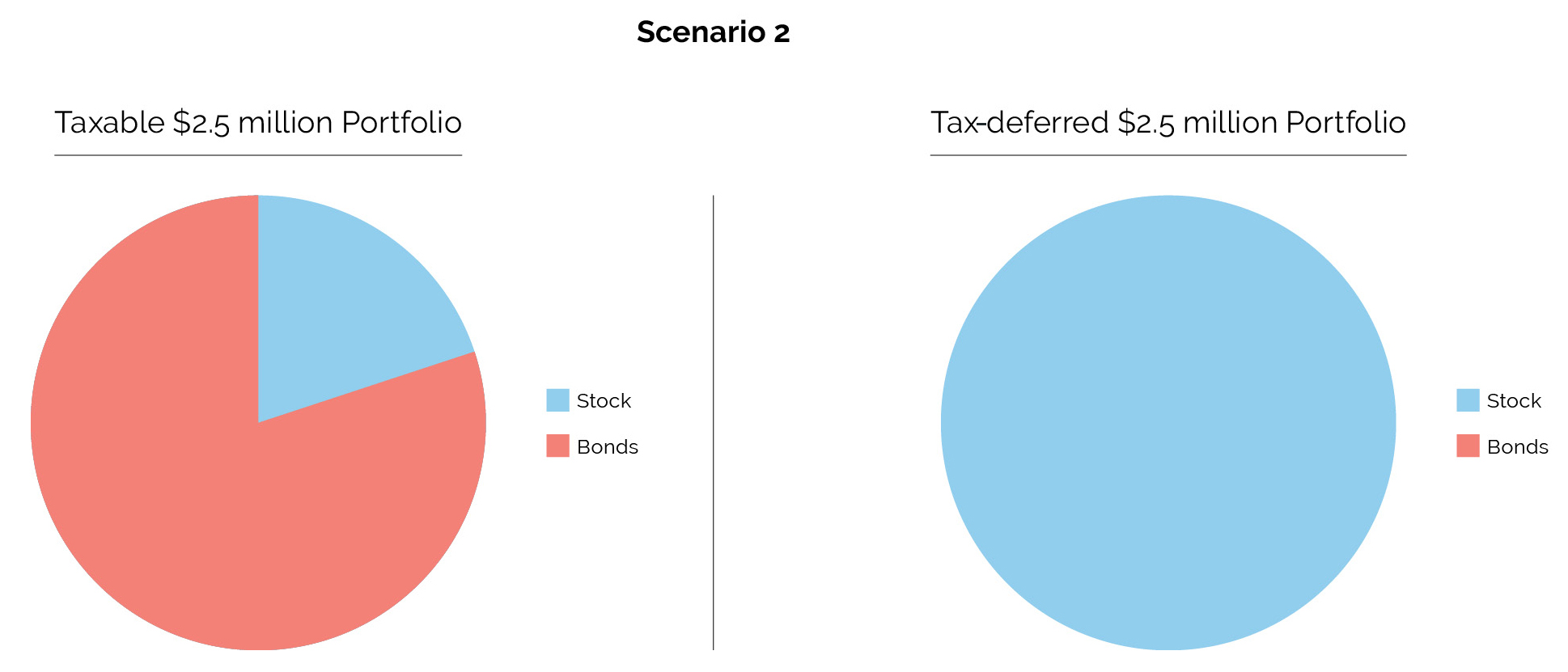

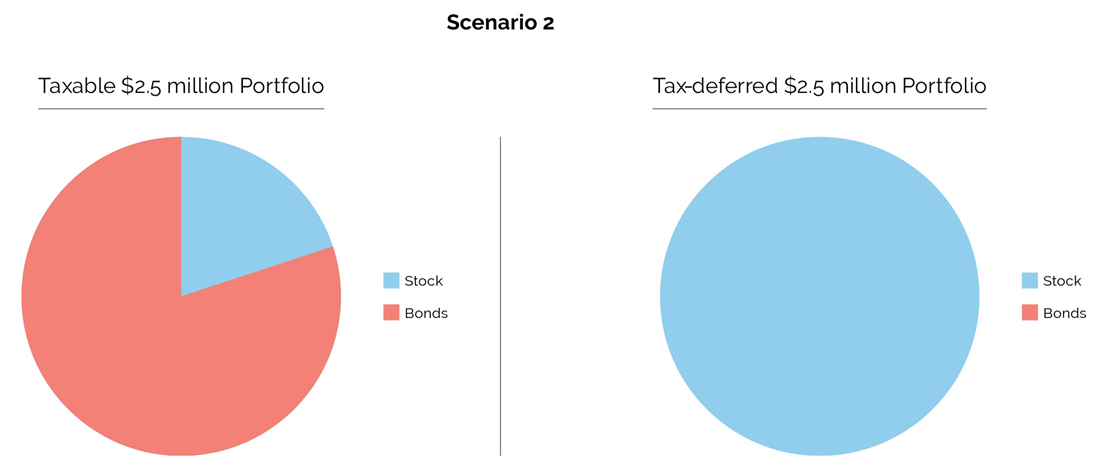

Location investing would dictate swapping taxable bonds for municipal bonds and locating as much of the municipal bonds as possible in the taxable portfolio, while placing as much of the high tax-sensitive assets (stocks) in the tax-deferred vehicle.

[5]

The aggregate 60% stock/40% bond allocation is the same in Scenario 2 as Senario 1, but the assets are located according to tax sensitivity. As a result, of the client’s $3 million in stock, only $500,000 is exposed to taxes resulting, in this example, in only $5,000 in taxes. The bulk of the tax-exposed assets are municipal bonds resulting in no tax on bond income. On a pre-tax basis, portfolio return is similar between Scenario 1 and Scenario 2. However, Scenario 2 only generated $5,000 in taxes while Scenario 1 generated $23,420 in taxes – a meaningful difference.

Location investing is optimal when including Roth IRAs that have tax-free distributions. However, traditional IRAs become less optimal when taxable required minimum distributions (RMD) begin.

Conclusion

At Cambridge Trust, we employ typical techniques such as tax-loss harvesting, municipal bonds and gifting to minimize our client’s tax burden and, where appropriate, implement more sophisticated strategies such as NUA management,

New Hampshire trusts and location investing. We are happy to talk to you and your accountant to see which approaches are best for you.

[1] Jenna L. McNamee, Getting Back on Track: A Guide to Smart Rebalancing, The Vanguard Group, 2019

[2] $75,000 of realized gains on a $1.5 million stock portfolio would not be unusual in a strong equity market.

[3] For purposes of this example, we are assuming the client is in the highest tax bracket for federal income taxes and capital gains. This is not uncommon for clients with $5 million in investable assets.

[4] Bond income is taxed at ordinary income tax rates, which in this case, includes the 37% federal rate and the state rate, which we are assuming to be the Massachusetts state tax rate of 5.1%.

[5] It is also important to consider the tax consequences of transitioning from a traditional investment strategy to a location strategy. The bond swap as described could generate a possible taxable gain or loss.

This material has been prepared for informational purposes only and is not intended to provide, and should not be relied on for, tax, legal or accounting advice. You should consult your own tax, legal and accounting advisors before engaging in any transaction.This material has been prepared for informational purposes only and is not intended to provide, and should not be relied on for, tax, legal or accounting advice. You should consult your own tax, legal and accounting advisors before engaging in any transaction.