Economy & Markets

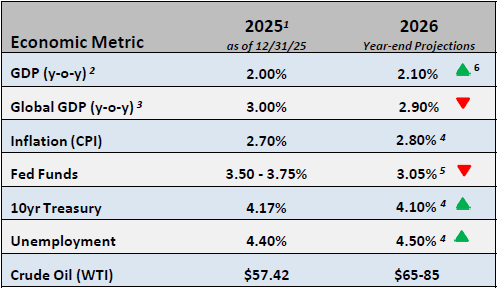

- In 2025, the U.S. economy surprised investors with its resiliency in the face of trade and tariff uncertainty in the first half of the year. Growth remained healthy through the second half of 2025 with third quarter GDP of 4.3% and continued strength expected in the fourth quarter, albeit with some moderation from the notable third quarter levels. This strength represents a tremendous shift from the recession fears back in April.

- As we begin 2026, our expectation is for the economy to continue growing in the 2.0%+ range. Consumer spending and business capital spending are expected to benefit from the One Big Beautiful Bill Act and will be something to keep a close eye on in the first half of 2026.

Equities

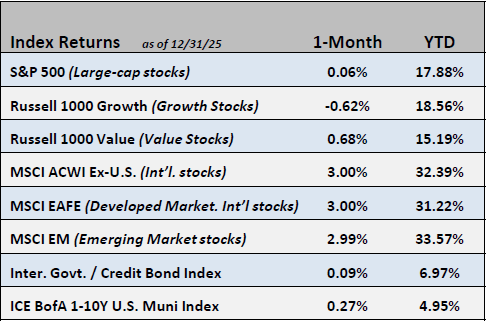

- To close out 2025 the S&P 500 was flat for the month of December but closed the year up +17.8%, the index’ third consecutive year delivering double-digit gains. In December, value-oriented stocks outperformed growth-centric names. Stocks in the financial and materials sectors led for the month while utilities, REITs, consumer staples and health care names all lagged. International stocks outperformed domestic equities in December.

- The S&P 500’s forward P/E multiple continues to trade at an elevated 22x as expectations for corporate earnings call for growth in FY’26 and FY’27 of +14.6% and +14.2%, respectively.

Fixed Income

- The yield curve continued to steepen (shorter maturity yields declined while yields on longer maturity bonds rose) following the Federal Open Market Committee’s 25 basis point rate cut.

- Investment grade credit spreads finished the year at 79 basis points. Although credit spreads remain historically tight, all-in yields are still attractive.

Employment

- Outside of the two most recent recessions, 2025 saw the lowest pace of average monthly job growth since 2003. Employers added 584,000 new jobs in 2025, averaging 49,000 per month. In 2024, the economy added nearly two million jobs or 168,000 per month.

- The December employment report showed that we ended the year with a 4.4% unemployment rate. We believe employment should improve in 2026 due to continued economic growth and the diminishing impact of tariffs on businesses.

Federal Reserve

- The choice of a new Chairman has dominated the headlines with an announcement expected shortly. No matter the choice, the new Chairman will face a difficult environment to navigate.

- Affordability has become a very important issue across the country, especially for the lower income cohort, as inflation continues to remain above the Fed’s 2% target. Real wage growth has been strong at 3.7% in December, providing some relief for workers.

Issues to Watch

- Geopolitics have dominated the headlines to start the year, with increased uncertainty from events in Venezuela, Iran, Greenland, Ukraine and elsewhere.

- Nineteen states raised their minimum wage on January 1st which provided a raise to 8.3 million workers. Thirty states now have a higher minimum wage than the federal minimum of $7.25.

1 Data provided by Bloomberg. Metrics are as of month-end or most recent publication

2 Provided by U.S. Real GDP Economic Forecast Survey Median

3 Provided by World Real GDP Economic Forecast Survey Median

4 Provided by Bloomberg Intelligence Forecast

5 Provided by World Probability Forecast

6 Arrows represent a month-over-month change

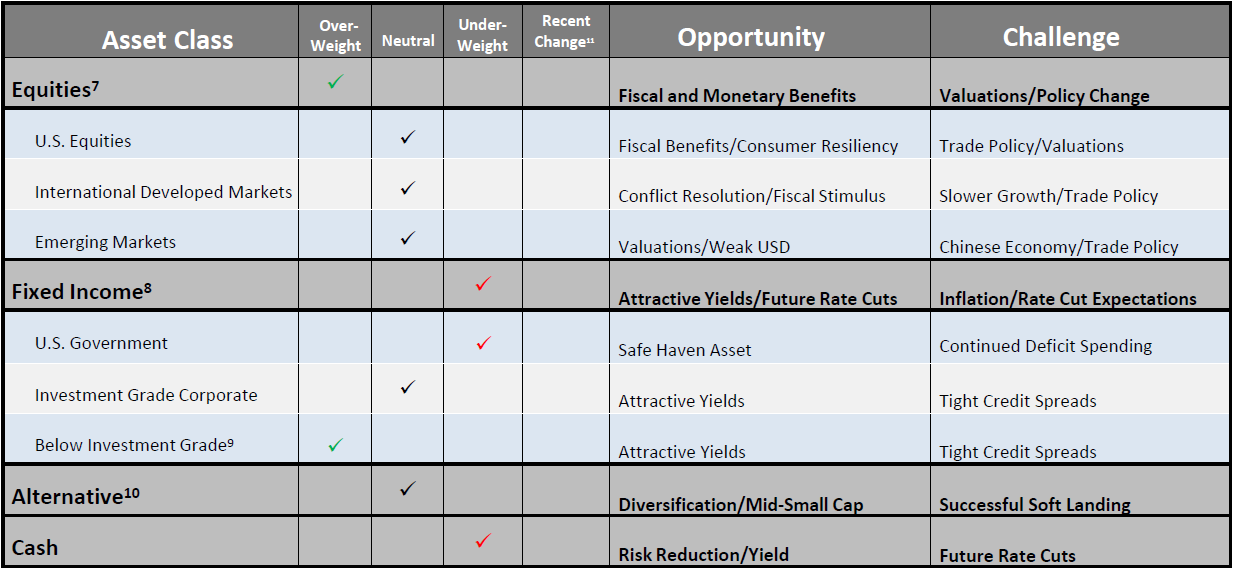

Asset Allocation / Tactical Positioning

7 Equity tactical weights are relative to the Cambridge Trust Wealth Management Core Equity allocation and is comprised of 80% S&P 500 and 20% MSCI AC World ex-U.S. Index.

8 Fixed Income tactical weights are relative to the Cambridge Trust Wealth Management Core Taxable allocation and is comprised of 100% Barclays Intermediate Gov/Credit Index.

9 Below investment grade holdings include high yield and emerging market debt mutual funds. Represents an out-of-benchmark allocation that will be reflected as an overweight position relative to the Barclays Intermediate Gov/Credit Index if any allocation is held.

10 Alternative tactical weights represent an out-of-benchmark allocation that will be reflected as an overweight position when utilized and neutral position when not.

11 Direction arrow highlights any recent changes of the overall allocation after a recent tactical asset allocation or strategy change. Last changes were made at January 2026 Asset Allocation Committee meeting.

Views are as of January 2026 and are subject to change based on market conditions and other factors. The opinions expressed herein are those of the author(s), and do not necessarily reflect those of Eastern Bankshares, Inc., Eastern Bank, or any affiliated entities. Views and opinions expressed are current as of the date appearing on this material; all views and opinions herein are subject to change without notice based on market conditions and other factors. These views and opinions should not be construed as a recommendation for any specific security or sector. This material is for your private information, and we are not soliciting any action based on it. The information in this report has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is neither representation nor warranty as to the accuracy of, nor liability for any decisions made based on such information. Past performance does not guarantee future performance.