As the holiday season approaches, Cambridge Trust Wealth Management would like to reflect on a momentous 2024. Over the past year we’ve increased the breadth of expertise within the Financial Planning Group, partnered with a 3rd party to strengthen our risk management analysis, and have enhanced our overall client experience.

While performing your year-end Financial Planning review, we recommend that you keep the following strategies in mind.

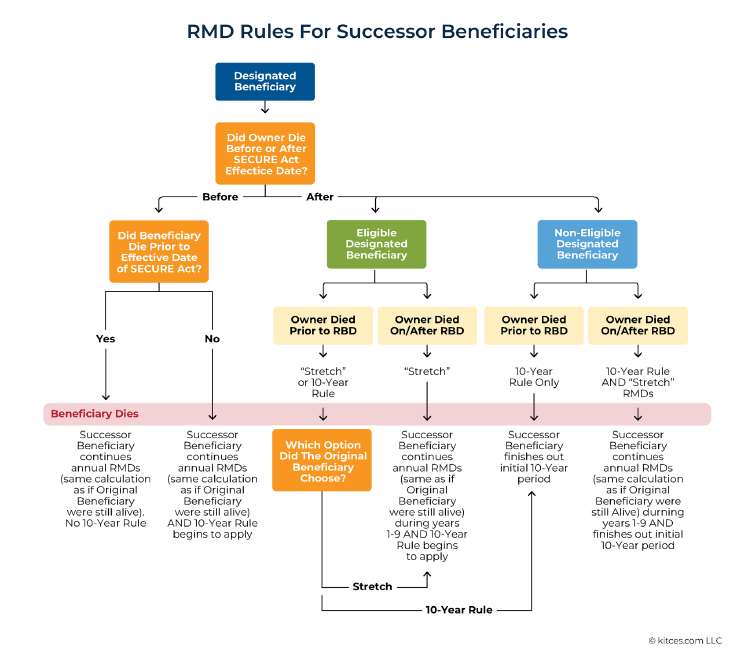

Retirement accounts distributions

In 2024, the IRS issued final regulations implementing legislative changes to the required minimum distribution (RMD) rules. Previously, RMD rules were amended by the SECURE Act of 2019 and the SECURE 2.0 Act of 2022.

The new regulations will require certain beneficiaries to take required minimum distributions from an Inherited IRA, while also being required to deplete the entire Inherited IRA within 10 years following the original IRA owner’s year of death. This rule would impact beneficiaries of deceased IRA owners who pass away on/after the required beginning date (the original owner began taking their RMD’s prior to death) and who are considered “Non-Eligible Designated Beneficiaries”.

Eligible Designated Beneficiary – Surviving spouse, disabled persons, chronically Ill persons, persons not more than 10 years younger than the decedent, minor children, some see-through trusts

Non-Eligible Designated Beneficiary – most non-spouse beneficiaries, some see through trusts

Non-Designated Beneficiary – charities, estates, non-see-through trusts

The IRS waived this requirement for calendar years 2021-2024. So, any inherited IRA account holder who failed to take an annual RMD in those years would not be assessed an excise tax for failing to do so. These beneficiaries must begin taking RMDs in 2025 based on their life expectancy and liquidate the account by the 10th year following the year of death of the original IRA owner.

Consult your tax advisor if you have questions about whether you should take a required distribution from your Inherited IRA before the end of 2024 and annually thereafter.

Retirement account contributions

The maximum contribution to your retirement plans for 2024 is $23,000 if you are under 50 years of age. If you are age 50 or over, you can take advantage of the catch-up contribution allowing you to contribute an additional $7,500. Maximum contributions for 2025 will increase to $23,500 and catch-up contributions will remain at $7,500.

The annual contribution limit for traditional or Roth IRAs is $7,000 for both 2024 and 2025, with an additional $1,000 catch-up if you are age 50 or over. Contributions are subject to income limitations, as well as earned income eligibility.

Looking ahead to 2025, participants between the ages of 60-63 will have the opportunity to take advantage of additional contributions through their defined contribution retirement plan. Individuals who turn 60, 61, 62, or 63 (for tax year 2025 only) may use an alternate increased amount of $11,250, giving the ability to contribute an additional $3,750 to their employer sponsored plan.

Health savings account (HSA)

If you are currently enrolled in a high-deductible health insurance plan, you qualify for an HSA. An HSA is a tax-deductible savings vehicle established to set aside funds to pay for healthcare expenses. Unlike flexible spending accounts (FSA), unused funds roll over and accumulate for use in future years. Instead of using your HSA as a savings account, consider leveraging it as another long-term investment tool. An HSA offers multiple tax benefits in the upfront tax deduction, tax deferred growth, and tax-free distributions for qualified health expenses. Most Health Savings Accounts allow you to invest a portion of your funds after meeting account balance requirements. HSA funds can be used at any time for qualified medical expenses, including retirement. Contribution limits vary based on coverage, the 2024 annual caps on deductible contributions are $4,150 for single coverage and $8,300 for family coverage. The catch-up contribution for an HSA is $1,000 if you are age 55 or older. In 2025, HSA contribution limits will increase to $4,300 for single coverage and $8,550 for family coverage.

Annually Review Your Beneficiary Designations

Each year brings the possibility of going through family and/or monetary changes that may warrant a review of your beneficiary designations. For example, a divorce, birth, or death in the family, receiving an inheritance or retiring are pivotal moments to review the beneficiaries on your financial accounts.

Keep in mind, beneficiary designations supersede other estate planning documents regarding the transfer of financial assets. So, it is extremely important to confirm all designations are current to ensure your wishes are met after you pass away. Take the time to review beneficiaries on employer retirement accounts, personal retirement accounts, HSA’s, and both personal and employer offered life insurance policies. In some cases, non-retirement investment accounts may also have a beneficiary designation known as “TOD” or transfer-on-death. Similarly, bank accounts may have a “POD” or payable-on-death designation.

Estate Planning with the New Hampshire Trust Advantage

Establishing and updating your Estate Plan will ensure assets are distributed according to your wishes after you pass away or become incapacitated. A properly executed Estate Plan can simplify the process for beneficiaries while providing clarity & reassurance for the Donor. At a minimum, a basic Estate Plan should include a Will, a Health Care Proxy & Medical Directive, and a durable power of attorney. In many cases, a Revocable Trust may provide an additional level of customization for the disposition of assets at death.

Following Eastern Bank’s acquisition of Cambridge Trust Company earlier in 2024, clients may also consider the New Hampshire Trust Advantage. New Hampshire offers some of the most favorable and flexible trust laws in the country. The New Hampshire Trust Advantage allows for a settlor (the person who establishes a trust) to create asset protection trusts and retain certain rights, powers, and interests. Additionally, there are tax advantages for non-grantor trusts.

If you do not have an estate plan, you should consider drafting documents with an estate planning attorney.

Gifting Strategies

Philanthropic gifting during your lifetime can reduce your overall tax liability while allowing the donor to see the positive impact of their gift. With strong market performance in 2023 and 2024, investors may consider the following:

Gifting low cost-basis assets: Gifting highly appreciated assets to a registered 501(c)(3) charity of your choosing is an effective way to reduce your potential capital gains tax liability. The charitable deduction for cash donations in 2024 is limited to 60% of the Donor’s AGI (adjusted gross income), or 30% of the Donor’s AGI if donating appreciated assets.

Qualified Charitable Distribution (QCD): Investors who are concerned about paying taxes on their Required Minimum Distributions may consider a Qualified Charitable Distribution. A QCD allows you to distribute up to $105,000 (in 2024) to qualified charities without including the distribution in your gross income. The charity receives a tax-free donation, and the donor can reduce their tax liability.

Donor-Advised Fund (DAF): A Donor-Advised-Fund is a charitable giving vehicle that allows you to contribute multiple years of donations into the fund in a single year and take the tax deduction in that year. A DAF offers the Donor flexibility in deciding on the timing of when assets are distributed from the DAF to the charity in subsequent years.

In 2024, the annual exclusion for gifts is $18,000 and the lifetime exemption amount is $13.61 million. In 2025, the annual exclusion amount is expected to increase to $19,000 and the lifetime exemption amount is expected to increase to $13.99 million.

Tax

Tax-loss harvesting: You may consider strategically realizing losses in your portfolio to offset realized gains. This requires close attention to both long-term and short-term holding periods for securities as well as a thorough understanding of the impact to your overall allocation. We strongly suggest working with your CPA and Investment Team for this approach.

529 Plans: Earnings in a 529 Plan grow tax-deferred and withdrawals are tax-free provided the funds are used to pay for qualified education expenses. In 2024, you can contribute up to $18,000 ($36,000 for couples splitting gifts) for a single year. You can also front-load 529 Plans by gifting 5-years’ worth of contributions or $90,000 ($180,000 for couples splitting gifts). In certain states, donors may benefit from a limited state income tax deduction on the gift.

Tax Cuts & Jobs Act: This bill, originally passed by Congress in 2017, made numerous temporary changes to Federal tax law including the reduction of tax rates for individuals and corporations, increasing the standard deduction and family tax credits, and limiting State and Local Tax deductions (SALT), amongst a litany of other changes. This bill was expected to sunset at the end of 2025, however, with the Republican party securing the White House and both chambers of Congress there are many questions about whether this bill will be extended, or a new piece of tax legislation proposed. It is simply too early to determine how this may play out. We’ll have to wait until next year for more information.

Credit Monitoring/Identity Theft

If you haven’t already done so, we recommend you take some time to check the accuracy of your credit report. To obtain a copy of your credit report, contact: Equifax Consumer Information Services Inc, Experian, or TransUnion LLC. Everyone is entitled to a free credit report once a year. If there are inaccuracies, we recommend you work with your creditor to ensure the accounts listed are in fact your own, and not fraudulently opened.

Identity theft can cause loss of financial assets, ruin your credit and be a major drain to your time and resources. Preventing it should be a priority. Consider following the best practices below to help you prevent identity theft:

Obtain identity theft protection. There are many identity theft protection services available to individuals. By taking advantage of one of these services you have an additional line of monitoring of your identity and credit.

Consider a digital vault. A digital vault is a secure online platform where you can store important digital documents, including a password manager to store your digital footprint in one place. In the event of death or disability, you can assign access to specific family members or power of attorney as you see fit.

Protect your social security number. Your social security number is the most useful to thieves when stealing your identity. You can reduce the risk of having your social security number stolen by not carrying it with you, avoiding listing it on applications unless necessary, and not providing it over the telephone or written communication to any institution with which you do not already have a relationship.

Monitor your bank account frequently. This will help you detect fraud early and stop it before it happens.

Reduce paper transactions. Studies have shown that 10% of all theft occurs through mail or trash. Elect to receive your statements electronically whenever possible. If you are receiving paper statements, be sure to shred or destroy them prior to discarding.

Cambridge Trust Financial Planning Group

Will Fleming CFP®, CTFA

Vice President | Manager of Financial Planning

[email protected]

Roshni Patel

Vice President, Financial Planning Officer

[email protected]

Flip Ruben CFP®

Senior Vice President, Senior Wealth Advisor & Senior Financial Planner

[email protected]

Cambridge Trust Wealth Management is a division of Eastern Bank. Views are as of December 2024 and are subject to change based on market conditions and other factors. The opinions expressed herein are those of the authors, and do not necessarily reflect those of Eastern Bankshares, Inc., Eastern Bank, Cambridge Trust Wealth Management, or any affiliated entities. Views and opinions expressed are current as of the date appearing on this material; all views and opinions herein are subject to change without notice based on market conditions and other factors. These views and opinions should not be construed as a recommendation for any specific security or sector. Employees and representatives of Cambridge Trust Wealth Management and Eastern Bank do not provide tax or legal advice. This material has been prepared for informational purposes only and should not be relied on for tax, legal, or accounting advice. You should consult your own tax or legal advisors concerning the application of tax laws to your particular situation. This material is for your private information, and we are not soliciting any action based on it. The information within has been obtained from sources believed to be reliable but its accuracy is not guaranteed. There is neither representation nor warranty as to the accuracy of, nor liability for any decisions made based on such information. Past performance does not guarantee future performance. Investment products are not insured by FDIC or any federal government agency. Not deposits of or guaranteed by any bank. May lose value.