“I can’t control the wind, but I can adjust the sail.”

– Ricky Skaggs

The ebb and flow of market psychology was on full display in 2025. While sentiment and consumer confidence were in the doldrums, consumption trends were firm and economic growth was surprisingly strong - highlighting the growing divide between soft sentiment indicators and hard economic data. Despite uncertainties surrounding tariffs, geopolitics, a government shutdown, and increasing fears of an Artificial Intelligence (AI) bubble, market resiliency rewarded investors with another strong year of returns across most major asset classes.

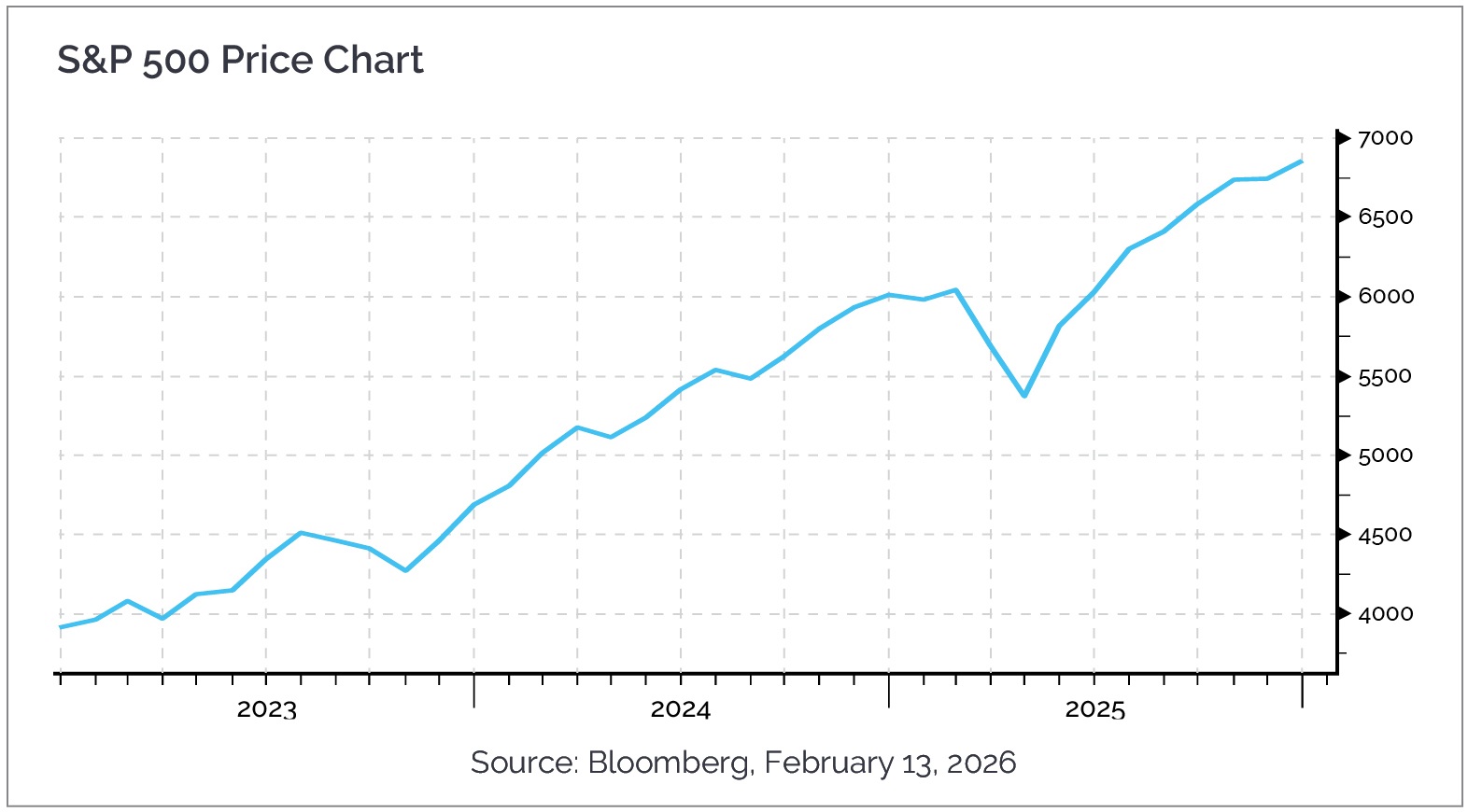

In 2025, the S&P 500 Index registered its third consecutive year of double digit gains, rising 17.9% and bringing the three year cumulative return for large capitalization U.S. stocks to nearly 86% (including dividends), 22.9% compounded annually. Markets have surged over the past three years, providing investors with substantial gains, and, in many cases, sizable capital gains tax liabilities. A first world problem.

But it wasn’t just large U.S. companies that performed well. The MSCI Emerging Markets Index rose more than 30%, while developed markets (ex U.S.) were not far behind. International equities outperformed the S&P 500 for only the third time since 2011 (2012, 2017, and 2025), following more than a decade of cumulative underperformance. Catalysts included improving local fundamentals, increased domestic investment in response to U.S. tariff pressures, attractive relative valuations, and a notably weaker U.S. dollar—which declined meaningfully against a basket of global currencies last year.

Volatility was rewarded and defensiveness was left behind. Cyclical stocks, speculative segments of the market, and lower quality companies delivered some of the strongest returns in 2025. As the Federal Reserve began cutting rates in the fourth quarter, small capitalization stocks also gained momentum, finishing the year with double digit returns. Gold once again stood out as a top performing asset, supported by central bank buying and investors seeking portfolio insurance. Overall, it was another positive year for risk assets, with strong performance across nearly all asset classes despite elevated political and economic uncertainty.

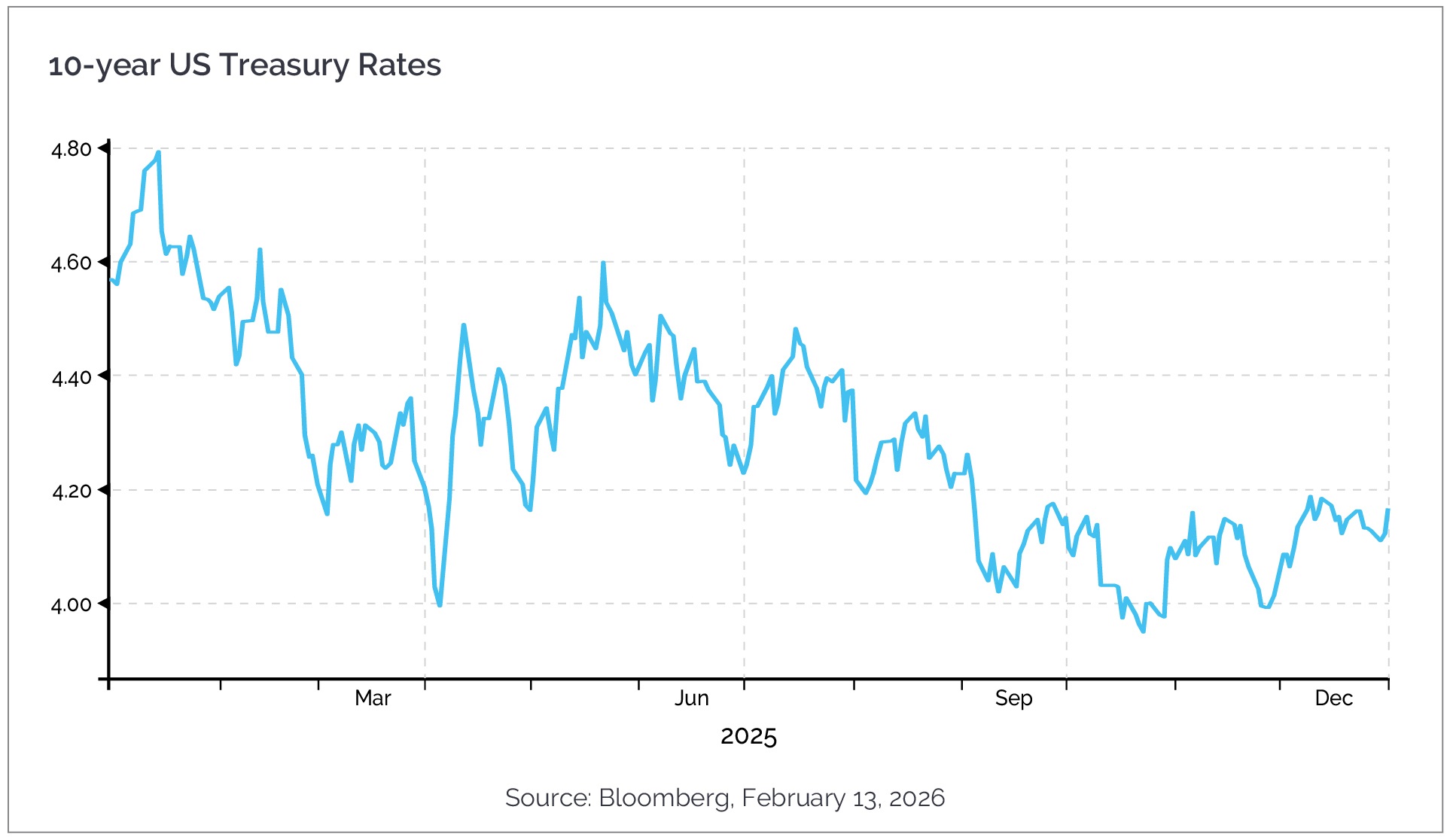

Fixed income also delivered solid results, with lower yields and tighter credit spreads driving returns. The Bloomberg Aggregate Bond Index gained 7.3% for the year. Despite ongoing concerns about federal debt and deficits, 10-year U.S. Treasury yields remained largely range bound throughout 2025. Tight credit spreads continue to signal confidence in corporate balance sheets and the broader economic outlook. The combination of moderating inflation, Fed easing, steady credit fundamentals, and strong demand for yield created a constructive backdrop for fixed income investors.

As the calendar turned from 2025 to 2026, much remains the same. Through January 2026, upward momentum in global equity markets has continued, with stocks across regions grinding higher. Domestically, major equity indices—including large cap, small cap, growth, and value benchmarks—are trading near all time highs. The same is true for most developed and emerging international markets.

In early February, the Dow Jones Industrial Average surpassed 50,000, while the Dow Jones Transportation Average also reached an all time high. According to Dow Theory, confirmation between the industrial economy and transportation activity has historically been associated with a healthy macroeconomic backdrop - though it is best viewed as a long term confirmation tool rather than a short term market signal.

2026 Outlook – A High Bar But Attainable

As with any annual forecast, we are reminded that markets can be unpredictable over shorter periods of time. Corrections and pullbacks are a normal part of investing and introduce uncertainty into any near term outlook. Political division and policy uncertainty remain important wildcards in the months ahead. Our objective is not to forecast with precision, but to remain directionally aligned with the dominant trends shaping the investment landscape.

In the U.S., market momentum continues to be supported by a combination of solid corporate earnings growth, strong profit margins, moderating inflation, and supportive monetary and fiscal conditions. While the labor market bears close monitoring, an unemployment rate near 4% and steady wage growth continue to support consumption, particularly among middle and upper income households.

Internationally, lower interest rates, improving earnings growth, attractive relative valuations, and currency tailwinds from a weaker U.S. dollar should continue to support foreign equity markets, as they did in 2025. That said, dollar weakness has become a consensus view and bears watching.

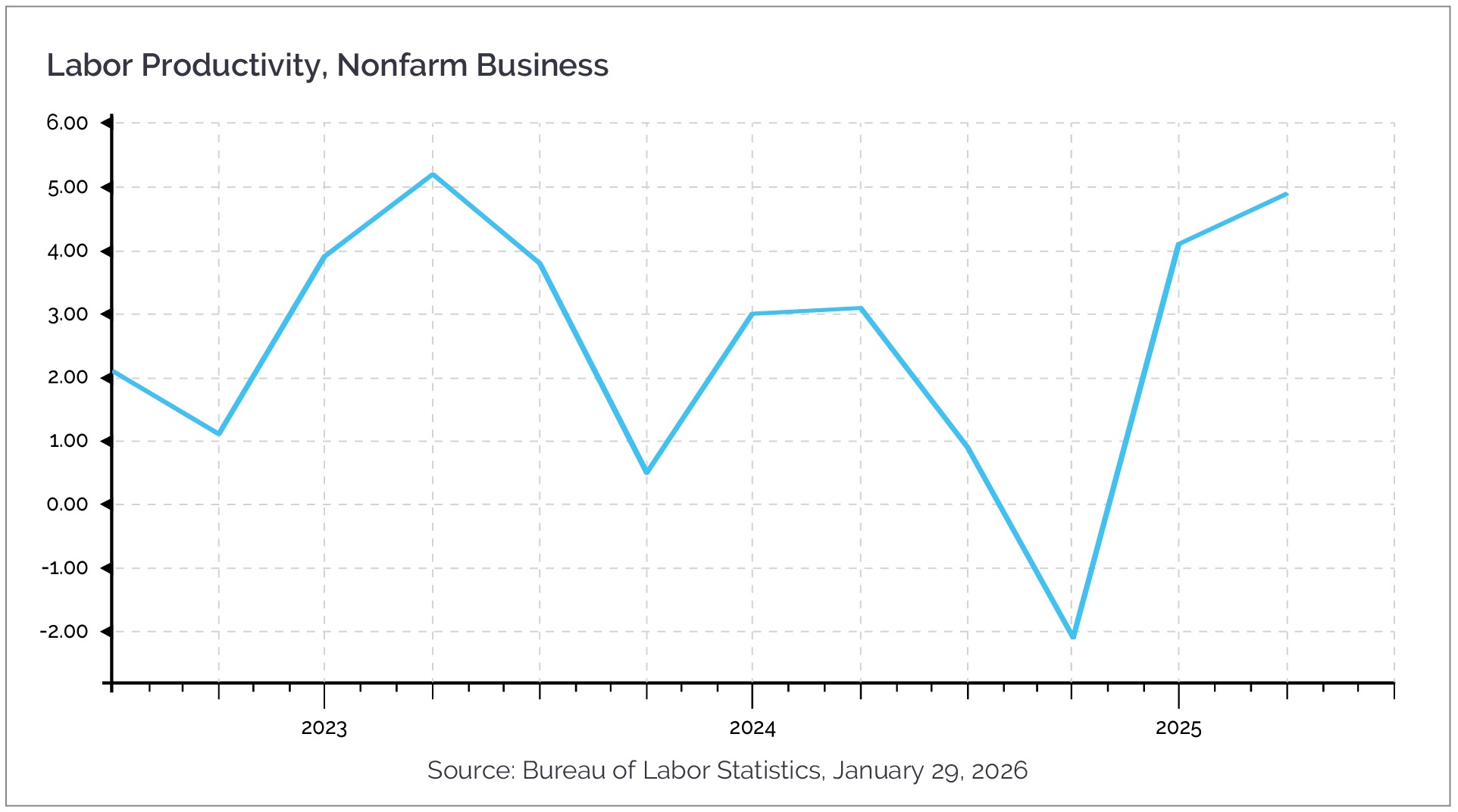

Economic growth in 2026 is expected to remain resilient, with real GDP projected in the low to mid 2% range—an acceleration from 2025. Productivity growth has improved meaningfully, supporting expansion even amid modest job creation. After several years of contraction, manufacturing activity has also shown signs of stabilization, with recent survey data pointing back toward expansionary territory.

Looking ahead, we are focused on five economic themes likely to shape outcomes in 2026:

- The path of interest rates and Federal Reserve policy

- The sustainability of the AI investment cycle

- Inflation trends

- Fiscal and monetary stimulus

- Labor market dynamics

Artificial Intelligence: Secular Force, Cyclical Expression

The artificial intelligence revolution has reshaped the investment landscape, driving strong returns across semiconductors, cloud infrastructure, and many related industries. Since late 2022, AI exposed companies have accounted for a substantial share of the S&P 500’s gains, with a small group of mega cap firms emerging as primary beneficiaries.

Investment in AI infrastructure remains robust, supported by aggressive capital spending from hyperscalers and cloud computing providers. This investment cycle has meaningfully contributed to economic growth and corporate earnings, but it has also increased market concentration, with a narrow group of technology oriented companies accounting for a disproportionate share of index level earnings growth.

It is important to distinguish between AI as a long-term secular force - likely to drive productivity, innovation, and economic growth for years - and AI related equities, which are subject to cyclical swings in sentiment, capital spending, and valuation. As financing conditions have tightened, markets have become more discerning about which companies can sustain growth without excessive leverage, creating periodic dislocations within the sector.

While it is too early to definitively identify the long term winners and losers, AI remains an area requiring disciplined oversight, valuation awareness, and active risk management.

Building a Weather-Proof Portfolio

The quote at the beginning of this piece resonated with me, as it reflects the strategic adjustments we made in client portfolios throughout 2025 and early this year. These were not wholesale changes, but incremental refinements - much like a sailor tacking gradually as winds shift. As conditions evolved, we adjusted portfolios by:

Taking Profits in Winners – The Discipline of Realization

While long term conviction is essential, realizing gains is a strategic necessity. Capital gains only become useful when realized, and disciplined profit taking allows for redeployment into attractively valued or less correlated opportunities.

Diversification – Beyond the AI Titans

The S&P 500 has become increasingly concentrated, with its largest constituents representing a significant share of total market capitalization. Diversification is not simply about owning more securities - it is about owning assets that behave differently across market environments, including fixed income, real assets, international equities, and value oriented strategies.

Risk Control Through Position Sizing

Position sizing remains the first line of defense in volatile markets. Higher growth and higher volatility exposures require thoughtful sizing to limit drawdowns and manage portfolio level risk.

Strategic Portfolio Management

Being “responsibly bullish” means balancing conviction with caution. This includes trimming outperformers, reallocating toward underappreciated opportunities, managing correlated exposures, and stress testing portfolios across a range of economic scenarios.

Bullish - but Balanced

Successful investors focus less on predicting the direction of the wind and more on making steady progress towards their long-term investment goals. Time in the market has consistently proven more effective than attempts to time the market.

Our outlook for the U.S. economy, interest rates, and corporate earnings remain constructive. Tailwinds from easing monetary policy, fiscal support, and a resilient consumer continue to underpin our expectations.

AI is transforming industries and creating long-term opportunities. But responsible investing requires discipline - strategic realization of gains, diversification, risk control, and ongoing portfolio oversight. As we move deeper into the decade, the appropriate stance remains clear: stay bullish—but stay smart.

A balanced approach – one that acknowledges risk without fearing it – remains essential for long-term success. We may not control when the wind changes, but we continually adjust portfolios to navigate whatever conditions lie ahead.

As always, we welcome the opportunity to review your portfolio and discuss how your investment strategy aligns with the evolving economic landscape. Please don’t hesitate to reach out to schedule a conversation with your Portfolio Manager, Relationship Manager, or Wealth Advisor.

Cambridge Trust Wealth Management is a division of Eastern Bank. Views are as of February 2026 and are subject to change based on market conditions and other factors. The opinions expressed herein are those of the author(s), and do not necessarily reflect those of Eastern Bankshares, Inc., Eastern Bank, or any affiliated entities. Views and opinions expressed are current as of the date appearing on this material; all views and opinions herein are subject to change without notice based on market conditions and other factors. These views and opinions should not be construed as a recommendation for any specific security or sector. This material is for your private information, and we are not soliciting any action based on it. The charts presented within are for educational purposes only. The information in this report has been obtained from sources believed to be reliable but its accuracy is not guaranteed. There is neither representation nor warranty as to the accuracy of, nor liability for any decisions made based on such information. Past performance does not guarantee future performance.